Regulations

Navigating EU's Corporate Sustainability Reporting Directive (CSRD): A Guide for Sustainability Champions

August 28, 2024 | By Sophia Mwema

As the Corporate Social Responsibility Disclosure (CSRD) evolves, businesses acknowledge the significance of sustainability reporting in crafting their corporate narrative. Companies can fulfill regulatory obligations and harness sustainability as a driving force for enduring prosperity through transparency, accountability, and forward-thinking strategies.

Understanding the CSRD

The Corporate Sustainability Reporting Directive (CSRD) introduces extensive and comparable sustainability reporting for EU-based companies. Expanding on the groundwork established by the Non-Financial Reporting Directive (NFRD), the CSRD integrates sustainability reporting into the realm of financial disclosure.

Effective as of January 1, 2024, the directive initiates a staged rollout, beginning with larger enterprises, followed by listed SMEs, and extending to non-EU entities with substantial operations within the EU.

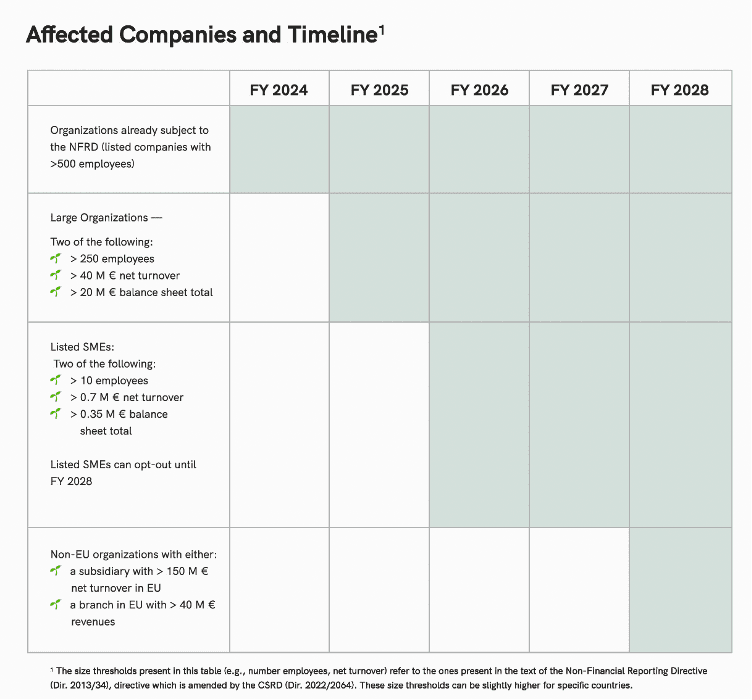

Timeline of affected companies within CSRD's scope

The double materiality principle within CSRD

The CSRD requires businesses to conduct double materiality assessments, which report on financial and impact materiality topics. This requirement is a revolutionary feature of the directive, as it acknowledges the impact of companies on the environment and society and the reciprocal influence of these factors on a company’s long-term viability.

The widespread adoption of IFRS, SASB, and TCFD illustrates the maturity and dominance of reporting on financial materiality, which addresses investors' interest in financial topics affecting an organization.

In contrast, reporting on impact materiality has lagged due to insufficient non-financial data and the fact that reporting has been optional. Impact materiality, as advocated in the GRI, addresses wider stakeholders' interests by reporting impacts on people and the planet.

CSRD requirements: the steps beyond compliance and toward strategic value

Double materiality provides insight into areas that pose risks, opportunities, and impacts to the organization and its stakeholders, used to design an effective, sustainable management system.

A comprehensive gap analysis is needed to evaluate existing sustainability reporting practices against CSRD requirements. Here, organizations lay the groundwork for action plans to enhance reporting effectiveness by identifying areas of strength and weakness. Companies taking a structured approach to navigate the complexities of the CSRD include:

Discovery process for sustainability context-setting. This exploratory phase is the basis of strategic planning. It involves assessing industry trends, analyzing internal policies and procedures, and engaging stakeholders to understand relevant environmental, social, and governance topics for the organization.

Define medium to long-term sustainability strategy. Analyzing the output from the discovery phase provides insight into the bi-directional impact between the company and its surroundings. Here, priorities surface upon examining the scale and scope of each material impact. Effective reporting happens when sustainability objectives align with the organization's strategy.

Implement measures to meet requirements. Strategy fosters clarity on actions to meet objectives and effectively engage stakeholders. Execution requires a concerted effort across all levels of the organization. From policy implementation, data aggregation, and capacity building to influencing behavior change, companies must invest in robust processes to fulfill reporting requirements and resulting improvements.

Compile sustainability report. Leverage digital solutions to streamline data collection and categorization as prescribed in the European Sustainability Reporting Standards (ESRS) under the CSRD. The required format is a single XHTML. Upon completing the earlier steps, the following inputs would be readily available for reporting - targets and goals, measures and KPIs, processes and controls, and improvement and review plans.

Obtain report assurance through third-party verification. An audit adds a layer of credibility to sustainability disclosures. The CSRD mandates audited verification of reported information. Audited reports reinforce the company's commitment to sustainability.

Embrace compliance as a strategic imperative by planning for improvements in your reporting. CSRD compliance allows sustainability leaders to evaluate the organization's progress toward goals by using feedback loops to inform operations, evaluate performance through periodic stakeholder forms, and actively adjust strategies accordingly.

Addressing potential pitfalls in corporate sustainability reporting

Despite the noble intentions of sustainability reporting, even the most well-resourced organizations face many challenges in ensuring the integrity of the disclosure. It falls upon those entrusted with steering the sustainability reporting within their organization to pay astute attention as they oversee the undertaking so that:

The initiative has more than a checklist approach but a targeted strategy for enhancing reporting capabilities. A profound understanding of organizational dynamics and sustainability goals is necessary.

Resourcing is a delicate balance between competing priorities - reporting obligations and implementing sustainability initiatives. Sustainability efforts can only succeed with adequate support and investment. Bridge this gap by strategically aligning resources with organizational sustainability objectives.

The quest for perfection does not hinder action. Iterate, start small, and enhance reporting practices over time. Sustainability is a journey marked by continuous improvement, not immediate perfection.

The team overcomes analysis paralysis. The abundance of data and metrics in sustainability reporting can overwhelm even the savviest decision-makers. Again, strategically aligning the critical performance indicators (KPIs) with sustainability objectives can help organizations efficiently recognize actionable insights.

Disclosures truly depict the reality of an organization’s progress. Transparency entails showcasing achievements and candidly addressing the challenges and reasons behind any lack of progress. Resist the lurking temptation to lie by omission.

Sustainability reporting, and by proxy sustainability communication, has often been motivated by regulatory compliance or reputational enhancement. There is an opportunity to contribute to the well-being of society and the environment by shifting the focus on creating a positive impact through advocacy, influence, thought leadership, and industry/sectoral leadership.

It is, however, critical to truthfully represent the level of the organization’s sustainability ambition and commitment. With increasing sustainability regulations such as the CSRD, actions that merely meet the legal requirement must be communicated as such. Misrepresenting this fact leads to a disconnect between rhetoric and reality.

How are you prepared for when (not if) your company comes under the scope of CSRD?

As seasoned advisors, GO2 Markets Advisory is committed to supporting organizations in this transformative journey, guiding them toward compliance and unlocking the strategic value inherent in sustainability reporting.

Contact us at advisory@go2-markets.com to navigate the nuances of sustainability compliance requirements more effectively and efficiently by leveraging specialized knowledge and resources. We help you select suitable approaches to ensure reliability and streamline data collection processes and analysis, saving you time and resources and maximizing accuracy.

With better preparedness, your organization can plot a path toward meaningful sustainability outcomes and earn the trust of stakeholders in the process.

The table below describes the scope of the CSRD:

Related articles

Understanding EU's Corporate Sustainability Reporting Directive

This article unpacks the significance of CSRD for EU companies and its transformative impact on sustainabilityreporting.