Net Zero

Harnessing Value Chain Engagement For CSRD Compliance and Net-Zero Targets

October 8, 2024 | By Giuseppe Coppola

The need for organizations to include their value chain in their sustainability strategy has never been more critical.

Corporate Sustainability Reporting Directive (CSRD) compliance and net-zero targets require companies to adopt a comprehensive approach to understanding and managing their value chains regarding sustainable practices and greenhouse gas (GHG) emissions.

The CSRD expands the obligation of non-financial reporting to over 50,000 organizations and establishes a standardized reporting framework. At the same time, companies aiming to achieve net-zero emissions by 2050 through frameworks like the Science-Based Targets initiative (SBTi) must consider their entire value chain.

CSRD: Sustainability Reporting Across the Value Chain

The CSRD marks a significant shift in how organizations report on sustainability. For the first time within the European Union, companies required to prepare non-financial statements must follow specific standards, known as the European Sustainability Reporting Standards (ESRS), developed by the European Financial Reporting Advisory Group (EFRAG). These standards ensure greater consistency and comparability of sustainability disclosures across companies.

Additionally, under the CSRD, companies must have their non-financial information reviewed by an independent third party, mirroring the audit process for financial statements. This shift from the Non-Financial Reporting Directive (NFRD) underscores the increasing importance placed by European lawmakers on sustainability reporting.

A critical requirement of the CSRD is the inclusion of a company's entire value chain in its sustainability report. When conducting the Double Materiality analysis, companies must consider their entire value chain, extending beyond tier 1 suppliers—identifying

i) the environmental and societal impacts of the organization's activities and

ii) the financial risks and opportunities stemming from sustainability issues.

An example of value chain from a fashion retailer

Businesses must collect and report primary data from relevant partners after identifying the "material" impacts, risks, or opportunities within the value chain.

For the first three years of reporting, companies may rely on secondary data available in-house. However, beyond this period, they are expected to gather primary data from these value chain partners reasonably. Organizations may use secondary data or proxies, such as industry averages if this proves impossible.

Organizations must establish effective data collection and validation mechanisms across their value chains to meet these requirements, engaging suppliers and partners beyond tier 1. This includes tracking key sustainability metrics, such as carbon emissions, resource consumption, and labor practices. While this represents a significant investment, it offers process optimization and risk management opportunities. Enhanced visibility into the value chain can reveal inefficiencies, unlock cost-saving opportunities, and reduce various risks. Furthermore, this proactive approach strengthens relationships with partners. It improves the resilience of the business model, ultimately contributing to long-term sustainability and competitiveness.

By requiring companies to report on their value chains, the CSRD extends corporate accountability beyond direct operations. It encourages transparency and responsible practices throughout the entire network of suppliers and partners. This approach pushes companies to address environmental and social impacts wherever they occur, fostering a more comprehensive commitment to sustainability.

Net Zero Targets and Scope 3 Emissions

Net Zero means cutting greenhouse gas emissions to as close to zero as possible, with any remaining emissions re-absorbed from the atmosphere by oceans and forests. — Net-zero coalition. United Nations Climate Action.

In 2015, 196 countries signed the Paris Agreement, cementing the global commitment to limit warming below 2°C. Rapid decarbonization is essential across all sectors, with net-zero emissions to be reached by 2050.

Many companies publicly commit to net zero, often through the Science-Based Targets initiative (SBTi), a globally recognized framework that helps businesses align their climate strategies with the latest scientific understanding. SBTi provides clear guidance for setting emissions reduction targets that adhere to the Paris Agreement's goals.

Since 2015, the number of companies committing to net zero by 2050 has grown steadily. According to the United Nations' "Race to Zero" campaign, over 8,300 companies have made this pledge—a significant leap from just a few hundred in the years following the Paris Agreement. This rise reflects the increasing recognition of the role of businesses in tackling climate change and the urgency for concrete actions to achieve net zero.

For corporations, reaching net zero means drastically reducing greenhouse gas emissions and offsetting any remaining emissions with high impact removal carbon projects.

However, achieving net zero is highly complex due to the intricate structure of global value chains. Emissions are often embedded deep within multiple tiers of suppliers, many of whom need more tools or knowledge to track and reduce their emissions.

Engaging every company within the value chain, especially smaller suppliers, can be challenging as they may need more resources or incentives to adopt low-carbon practices. Moreover, corporations must account for emissions from various activities, from raw material extraction to product use, making accurate data collection and reporting difficult. Coordinating these efforts across diverse geographies with varying regulations adds another layer of complexity.

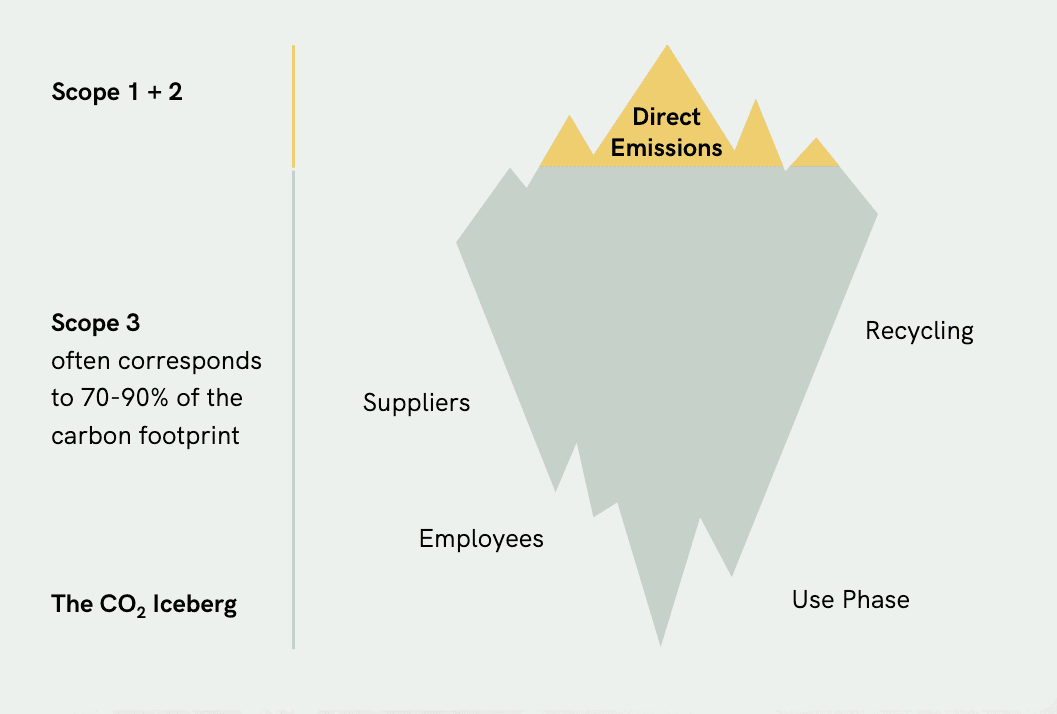

Upstream and downstream value chain emissions, categorized as Scope 3 emissions, account for 70-80% of a company's total carbon footprint. A significant reduction in Scope 3 is critical to reaching net zero.

Scope 3 emissions represent between 70 and 80% of the organization's total carbon footprint.

Reducing Scope 3 emissions entails a five-step process, with steps 2 through 5 being iterative:

Screen Scope 3 Emissions. Use the 15 categories the Greenhouse Gas (GHG) Protocol defines to identify your emissions. Assess the relevance of each category based on the organization's associated GHG emissions. Data typically available in-house, such as financial expenditures on goods and services, waste generated, and products sold, can be used for an initial estimation. Preliminary calculation will likely involve significant uncertainty. Gathering more accurate primary data from value chain partners can reduce uncertainty.

Map the Value Chain. Identify key value chain partners beyond tier 1 contributing significantly to Scope 3 emissions. For companies where upstream emissions dominate, a limited number of suppliers (often the top 150 by spend) may account for approximately 65% of total Scope 3 emissions.

Engage Value Chain Partners. Collaborate with relevant partners to collect primary data such as energy consumption, the share of revenues or costs the organization represents, and spending on products and services. Ideally, partners will have already developed a product carbon footprint for their goods or services.

Refine Scope 3 Calculation. Use the collected data to refine your Scope 3 emissions calculation to reduce uncertainty in your carbon footprint estimates. A lower uncertainty level is crucial for defining effective emissions reduction initiatives. The estimated emissions reductions of any proposed initiative must exceed the uncertainty margin to justify implementation.

Define Scope 3 Reduction Projects. Work collaboratively with key value chain partners to design projects to reduce their GHG emissions. Be prepared to provide financial and operational support to facilitate these initiatives. For example, encouraging partners to purchase and redeem energy attribute certificates, such as GOs or I-RECs, can help them decarbonize their Scope 2 emissions. If tier 1 partners are unwilling to cooperate, companies may need to explore switching to new suppliers with lower GHG emissions.

Get proactive about integrating the entire value chain.

Businesses proactively embracing these challenges will be better equipped to manage risks, seize opportunities, and contribute meaningfully to global sustainability goals. As regulations evolve and market demands for sustainability performance increase, companies can leverage their sustainability strategies as a competitive advantage and a driver of value creation.

At GO2 Markets, our Advisory team is committed to guiding organizations through this transformative journey, helping them navigate compliance while unlocking the strategic value of sustainable practices. Our expertise assists global companies in efficiently addressing Scope 3 emissions and effectively engaging their value chain partners. Whether seeking to achieve net zero targets or comply with sustainability reporting requirements, we provide tailored solutions that save your company time and resources while enhancing your competitiveness.

Watch the CSRD and Scope 3: Best Practices for Value Chain Reporting webinar to learn more about meeting CSRD requirements while aligning with stakeholder expectations to drive deeper decarbonization.

Related articles

Value Chain Engagement Strategies

This article provides actionable insights into the why, what, and how of value chain engagement in corporate sustainability.